Americans Recast China

Americans Recast China

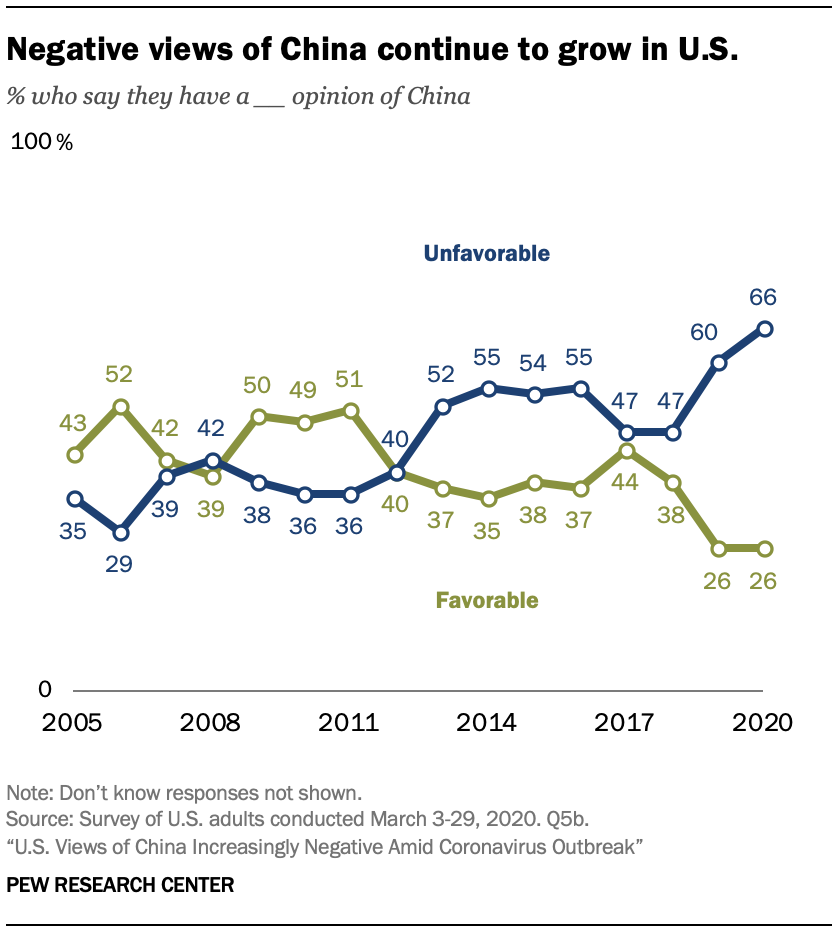

American views of China are no longer a niche polling story for diplomats and think tanks. They are becoming a market signal, a campaign issue, and a strategic constraint for companies that still assume public opinion can be managed with vague talk about globalization. The shift matters because perception now drives policy: tariffs, export controls, university partnerships, supply-chain moves, and even the language politicians use on the campaign trail. If your business touches manufacturing, semiconductors, higher education, media, or national security, this is not background noise. It is the operating environment. The bigger story is not simply that skepticism toward China exists. It is that the skepticism appears broader, more durable, and more politically useful than in earlier eras of U.S.-China tension.

- American views of China are increasingly negative, and that shift has consequences well beyond public opinion.

- Washington is likely to treat a tougher China posture as one of the few durable bipartisan positions left.

- Businesses face growing pressure to rethink supply chains, messaging, and geopolitical risk exposure.

- Public sentiment is turning into policy momentum across trade, technology, education, and security.

Why American views of China matter more than ever

Public opinion alone does not write foreign policy. But it sets the ceiling for compromise and the floor for confrontation. When voters grow more skeptical of a rival power, elected officials gain permission to sound tougher and lose incentives to defend engagement. That is especially important in the current U.S. climate, where bipartisan agreement is rare and political symbolism often becomes law.

The practical result is straightforward: American views of China now shape what is politically possible. A lawmaker can support tighter export restrictions on advanced chips, more scrutiny of land purchases, harsher review of academic ties, and broader industrial policy with relatively little fear of public backlash. For multinationals, that means geopolitical exposure is no longer just a boardroom risk model. It is a consumer and legislative issue at the same time.

When public distrust hardens, policy does not need a triggering crisis to move. It only needs an opening.

What is driving the shift

The deterioration in sentiment did not come from a single headline. It is the accumulation of several overlapping narratives, each reinforcing the other.

Security rivalry is now central

For years, many Americans understood China mainly through economics: low-cost manufacturing, trade imbalances, and the promise or threat of global competition. That frame has changed. Today, security concerns dominate. Taiwan tensions, cyber fears, military modernization, surveillance technology, and allegations of influence operations all push public perception away from commercial rivalry and toward strategic contest.

That matters because security narratives are stickier than trade narratives. Voters may accept trade-offs in the name of cheaper goods. They are far less likely to tolerate perceived vulnerability tied to national defense or critical infrastructure.

Economic frustration found a geopolitical target

China has also become a vessel for broader U.S. anxieties about lost industrial capacity, wage pressure, dependency on foreign manufacturing, and the fragility of global supply chains. Whether every complaint is economically precise is almost beside the point. Politics rarely waits for perfect calibration. Once a country becomes the public face of deindustrialization fears, leaders have a strong incentive to act visibly.

That is why reshoring, friend-shoring, and domestic industrial subsidies now carry emotional weight as well as strategic logic. They signal control. They tell voters that someone is reducing dependence, even if the underlying supply network remains deeply international.

The pandemic changed the emotional baseline

The pandemic left a residue of mistrust that extends far beyond public health. It intensified scrutiny of transparency, global dependencies, and institutional credibility. Even where details remain contested, the period helped cement a more adversarial baseline in American political culture. Once that baseline sets in, every subsequent flashpoint gets interpreted through the same lens: less benefit of the doubt, more assumption of competition.

How politics will weaponize American views of China

Expect this issue to remain politically irresistible. Toughness on China offers a rare combination in U.S. politics: bipartisan appeal, national-security framing, and economic populist language. That means candidates can use it to speak simultaneously to workers, defense hawks, tech strategists, and voters worried about American decline.

There is also a structural reason the rhetoric will continue. Taking a harder line on China often presents fewer immediate domestic costs than other foreign-policy positions. The language is simpler. The villains are clearer. The symbolic payoff is high. For that reason, even modest public skepticism can generate outsized political follow-through.

China is no longer just a foreign-policy file. It is an all-purpose domestic political argument.

That can produce blunt policy. Politicians do not always distinguish between legitimate security concerns, commercial interdependence, academic cooperation, and xenophobic overreach. This is where the conversation gets dangerous. Hardening public sentiment can support prudent resilience, but it can also flatten nuance and encourage performative escalation.

What businesses should read between the lines

Executives should resist the temptation to treat polling on China as abstract geopolitical mood music. It has direct operational consequences.

Supply chains face a perception test

Companies with deep manufacturing exposure to China are no longer dealing only with cost, efficiency, and logistics. They are dealing with reputation and policy risk. Investors, regulators, customers, and procurement partners increasingly want to know how dependent a firm is on any one geopolitical chokepoint.

The boardroom question is changing from Can we source efficiently? to Can we explain this exposure if tensions worsen?

Tech firms are in the hottest zone

Semiconductors, artificial intelligence, cloud infrastructure, telecom equipment, biotech, and advanced manufacturing sit at the center of U.S.-China tension. These sectors are where public skepticism and national-security policy overlap most aggressively. If you are building in any of these areas, expect more compliance complexity, more partner screening, and more pressure to map dependencies down to component level.

Pro tip: Companies should maintain an internal list of risk-sensitive assets such as chip design IP, training data pipelines, supplier concentration metrics, and cross-border research agreements. If public sentiment continues to deteriorate, these become first-order governance issues.

Universities and media institutions are not exempt

Public opinion shifts do not stay confined to factories and defense policy. Academic exchanges, student programs, research partnerships, and editorial decisions can all come under renewed scrutiny. Institutions that built their global strategy around open exchange may now have to prove they can separate openness from naivete.

That does not mean decoupling from every Chinese institution. It does mean governance must become more explicit. A vague commitment to international collaboration is no longer enough.

Why American views of China may outlast the current news cycle

One mistake analysts often make is assuming that public hostility peaks during moments of tension and fades when headlines cool. That may be less likely this time because the drivers are structural.

- Great-power competition gives the relationship a permanent strategic frame.

- Industrial policy ties China skepticism to domestic jobs and manufacturing revival.

- Technology rivalry raises the stakes around leadership in

AI, chips, and digital infrastructure. - Election incentives reward visible toughness and punish accommodation.

Put differently, this is not just about one incident or one administration. It reflects a broader rewrite of how the American public interprets power, dependency, and national resilience.

Where the story gets more complicated

A tougher public mood can be rational without being universally accurate. China is not a single-issue threat, and U.S. interests are not served by reducing every interaction to zero-sum confrontation. The danger is that public skepticism can erase distinctions that policymakers badly need.

Competition is real, but interdependence remains real too

The U.S. and China remain deeply linked through trade flows, financial systems, consumer markets, research ecosystems, and climate realities. Full decoupling is more slogan than plan. Even as businesses diversify, many still rely on Chinese manufacturing capacity, technical expertise, or consumer demand.

That is why serious strategy will likely look less like severance and more like selective insulation: protect sensitive sectors, diversify critical dependencies, and preserve channels where cooperation still serves national interests.

Public anger can drift into bad policy

There is also a line between vigilance and overreach. If policymakers collapse all China-related activity into suspicion, they risk chilling legitimate scholarship, punishing communities unfairly, and weakening the openness that historically powered U.S. innovation. A credible strategy has to defend security without undermining the pluralism and scientific exchange that make the U.S. competitive in the first place.

The smartest China policy is not the loudest one. It is the one that can tell the difference between exposure, competition, and hysteria.

What to watch next

If you want to understand where American views of China are heading, watch the translation from opinion to institution. The most revealing signals will not be speeches alone. They will be policy design, budget priorities, and compliance requirements.

Signals that matter

- Expanded export controls around advanced computing and semiconductor tooling.

- Stricter investment screening for sensitive sectors.

- More pressure on universities to audit foreign partnerships and funding channels.

- Procurement rules favoring domestic or allied sourcing.

- Campaign messaging that treats China as both an economic and cultural flashpoint.

Also watch corporate earnings calls. Executives may not make grand geopolitical declarations, but changes in language around regionalization, supplier diversification, inventory buffers, and country concentration risk are often the earliest signs of strategic adaptation.

The bottom line on American views of China

The broad shift in American sentiment toward China is not just a reflection of anxiety. It is becoming an organizing principle for policy, commerce, and political identity. That makes it far more consequential than a standard poll story. Once public opinion hardens at scale, institutions start to redesign themselves around it.

For policymakers, the challenge is balancing deterrence with discipline. For businesses, it is replacing wishful thinking with scenario planning. For universities and cultural institutions, it is preserving openness while proving they understand risk. And for the public, the real test is whether skepticism can stay grounded in strategy instead of sliding into reflex.

China will remain central to the American debate not because every voter tracks the details of bilateral relations, but because the country has become a shorthand for bigger fears: dependency, decline, lost leverage, and the race to define the next global order. Once a foreign rival starts carrying that much symbolic weight, the politics rarely soften on their own.

The information provided in this article is for general informational purposes only. While we strive for accuracy, we make no guarantees about the completeness or reliability of the content. Always verify important information through official or multiple sources before making decisions.