Oil Giants Cash In Amid Price Shock

Oil Giants Cash In Amid Price Shock

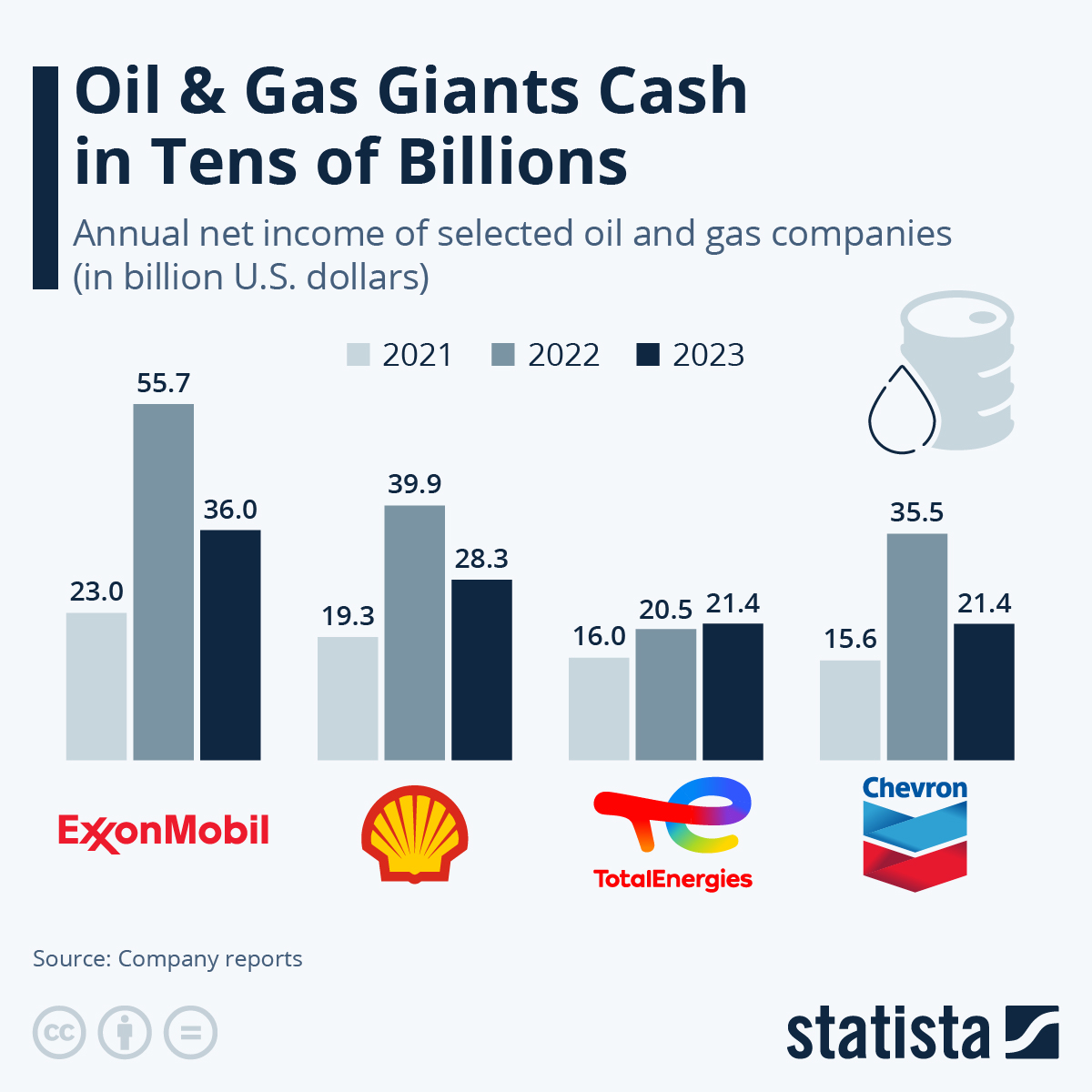

Oil company profits are surging again, riding a wave of volatile crude benchmarks and tight supply chains just when consumers expect relief at the pump. The tension is obvious: households are squeezed, governments warn about price gouging, and investors demand capital discipline while pushing for faster decarbonization. Yet the biggest integrated players are quietly printing record free cash flow, snapping up assets, and locking in long-term advantage. The stakes are high because oil company profits now shape everything from geopolitical alliances to the timeline for grid-scale renewables, and the current earnings cycle is exposing who is prepared for a messy energy transition and who is clinging to a fading playbook.

- Big oil is converting price volatility into resilient margins through trading desks and disciplined

capex. - Shareholder rewards via buybacks and dividends are colliding with political pressure for windfall taxes.

- Refining constraints and

OPEC+decisions are amplifying price swings that feed profits. - Carbon strategies hinge on using today’s cash to fund low-carbon bets without eroding returns.

How oil company profits spiked

Trading desks turned volatility into cash

When crude swings between WTI discounts and Brent premiums, integrated majors lean on their commodity trading arms. These desks arbitrage storage, tanker routes, and timing spreads, effectively monetizing chaos. Even as headline prices briefly cooled, firms locked in profits through hedges and contango plays, turning volatility itself into a profit center rather than a risk. That transforms traditional upstream exposure into a more diversified earnings engine, insulating income statements even if spot prices soften.

Disciplined capex kept margins fat

Unlike the last supercycle, leadership teams kept capex in a tight band, prioritizing short-cycle shale tiebacks and brownfield upgrades over mega-project gambles. With unit costs optimized and breakevens pushed below $40/bbl in some basins, every incremental dollar above that line flows straight to free cash flow. This capital discipline explains why profits are outpacing production growth – companies are squeezing more margin from each barrel instead of chasing volume for its own sake.

Refining constraints amplified the windfall

Refining capacity shuttered during the pandemic has not fully returned, creating persistent tightness in products markets. Crack spreads on gasoline and diesel widened, feeding downstream earnings even when crude prices dipped. Limited investments in new refineries – due to permitting friction and ESG scrutiny – keep the bottleneck intact. That downstream leverage is now a structural advantage for integrated firms, allowing them to capture margins across the value chain.

Key insight: Volatility is no longer just endured; it is engineered into the model. Trading-savvy majors are treating price swings as an asset class, not a headache.

Politics, pressure, and oil company profits

Windfall tax threats and policy crossfire

Governments facing voter anger are dusting off windfall tax proposals, arguing that extraordinary oil company profits should fund fuel subsidies or grid upgrades. Executives counter that punitive levies will chill investment and tighten supply further. The policy debate matters because sudden taxes can distort capital allocation, pushing companies to accelerate buybacks before rules change or to defer projects until fiscal terms stabilize. The risk: knee-jerk policy could undercut the very supply stability that policymakers demand.

Shareholder demands vs consumer pain

Boards remain under pressure to prioritize shareholder returns via dividends and aggressive buybacks. That capital return posture collides with consumer frustration over pump prices, painting companies as profiteers even when retail prices reflect broader supply-demand imbalances. The perception gap invites reputational risk and deeper scrutiny from antitrust regulators eyeing potential collusion in refining or distribution. Managing that optics problem requires clearer disclosure on pricing mechanics and investment timelines.

Geopolitics keeps the till ringing

Sanctions on certain exporters, cautious OPEC+ quotas, and maritime chokepoint tensions keep supply fragile. Every disruption nudges futures curves upward, reinforcing the profit machine. Integrated majors with diversified assets and storage can reroute cargoes quickly, monetizing dislocations. Smaller independents without trading heft cannot replicate that agility, widening the profitability gulf between supermajors and everyone else.

Where the cash is going

Balance sheets first, then buybacks

Most majors used the initial cash gush to deleverage, pushing net debt ratios below pre-pandemic levels. With balance sheets fortified, they shifted to aggressive buybacks, shrinking share counts to boost per-share metrics. Investors have rewarded the discipline, but the strategy faces political backlash if it appears to prioritize Wall Street over energy affordability. The balance between rewarding shareholders and demonstrating social license will define boardroom agendas this year.

Selective M&A bets on advantaged barrels

Rather than chasing volume, acquisitive moves are targeting advantaged barrels with low emissions intensity and existing infrastructure. Buying into mature basins with established midstream lowers execution risk and keeps breakevens tight. These deals show that oil company profits are being recycled into defensive growth, not reckless expansion – a lesson learned from the last boom-bust cycle.

Funding the low-carbon pivot without dilution

Companies are earmarking slices of free cash flow for CCUS, renewable fuels, and grid-scale storage. The trick is to fund these bets without eroding return on capital employed. Some are ring-fencing transition portfolios with separate hurdle rates and off-balance-sheet partnerships, treating them as venture-style options. Success hinges on translating oil company profits into durable advantages in power markets before subsidies taper and competition from utilities intensifies.

Pro tip: Watch capital allocation slides for clues: a rising share of growth dollars toward

CCUSand hydrogen signals real commitment, not just marketing.

Operational levers behind the surge

Digital twins and leaner rigs

Operational efficiency is multiplying profitability. Digital twin models and predictive maintenance reduce downtime on rigs and refineries, cutting operating expenses per barrel. Automated drilling programs in shale basins are compressing cycle times from spud to sales. These tech gains are wrapped in understated line items, but they underpin the margin expansion that makes oil company profits more resilient to price dips.

Supply chain control as a profit moat

After pandemic-era chaos, majors secured long-term contracts for critical equipment and shipping. Owning or controlling logistics removes middlemen, stabilizes costs, and allows faster arbitrage of regional price spreads. It also cushions the impact of labor shortages by smoothing project timelines. Supply chain discipline has become a stealth moat as much as any geological advantage.

Scope 1 and 2 emissions cuts guard market access

Many import markets are rolling out carbon intensity rules. Firms trimming scope 1 and scope 2 emissions through electrified operations and methane abatement are protecting access to premium buyers. That environmental hygiene is not just about reputation – it preserves price realizations and reduces the discount risk associated with carbon border adjustments.

Risks to the profit machine

Price whiplash and demand destruction

If high prices trigger demand destruction or a rapid EV adoption spike, the earnings party could cool fast. Refiners are particularly exposed if gasoline demand falls faster than expected while diesel margins compress. Hedging programs blunt the initial shock, but structural shifts in consumption would force a rebalancing of portfolios and possibly strand some high-cost assets.

Policy whiplash on climate and taxes

Uncertain regulatory timelines for methane fees, carbon pricing, and windfall taxes add planning risk. Delays in permitting for pipelines and carbon storage hubs can stall growth projects, while sudden policy shifts can reprice assets overnight. Boards are modeling multiple policy scenarios, but persistent uncertainty raises hurdle rates and may shrink investment appetites just when supply is needed.

Talent and technology gaps

As the energy workforce ages and tech companies lure digital talent, maintaining operational excellence is harder. Companies relying on legacy systems may struggle to scale data-driven efficiency gains. The long-term threat: margin erosion not from oil prices but from an inability to modernize quickly enough to keep costs low.

Future of oil company profits

Scenario: durable mid-cycle prices

If crude settles into a mid-cycle band with moderate volatility, expect sustained but less explosive profits. Companies will lean harder on trading to extract incremental value and on cost discipline to maintain margins. Shareholder returns will stay strong, but growth capex could creep up as confidence returns.

Scenario: accelerated transition shock

A rapid policy-driven pivot to electrification could compress demand faster than supply can adapt. In that case, the winners will be those who already used today’s oil company profits to build credible positions in power markets, biofuels, and storage. Laggards risk being stuck with cash-generating but depreciating assets.

Scenario: geopolitical supercycle

Persistent geopolitical risk could keep prices elevated for years, entrenching the profit surge. That would intensify calls for redistribution through taxes and could delay transition investments if boards prioritize near-term payouts. The strategic danger is missing the window to redeploy cash into future-proof businesses.

Why this matters: How companies deploy today’s windfall will determine whether they dominate a hybrid oil-and-electricity future or become cash-rich relics.

What to watch next

Capital allocation signals

Track the ratio of buybacks to growth capex in quarterly disclosures. A sustained tilt toward shareholder returns without scaled transition investment suggests confidence in long-lived oil demand but raises long-term risk.

Refining and petrochemicals pivot

Watch for investments in petrochemicals and lubricants that can absorb barrels even if transport fuels decline. These moves hint at a strategy to defend margins in a decarbonizing transport sector.

Grid and storage plays

Announcements of utility partnerships, grid-scale storage projects, or retail power offerings reveal how integrated players plan to evolve into full-spectrum energy providers. The timing and scale of these moves will show whether oil company profits are financing the transition or postponing it.

The bottom line: today’s profits are a stress test. The firms that treat volatility as an ally, invest in efficiency, and redeploy cash into low-carbon growth will write the next chapter of the energy economy. Those that simply harvest the cycle may find that the market, regulators, and customers move on faster than expected.

The information provided in this article is for general informational purposes only. While we strive for accuracy, we make no guarantees about the completeness or reliability of the content. Always verify important information through official or multiple sources before making decisions.