Oil Shocks Are Rewiring Geopolitics

Oil Shocks Are Rewiring Geopolitics

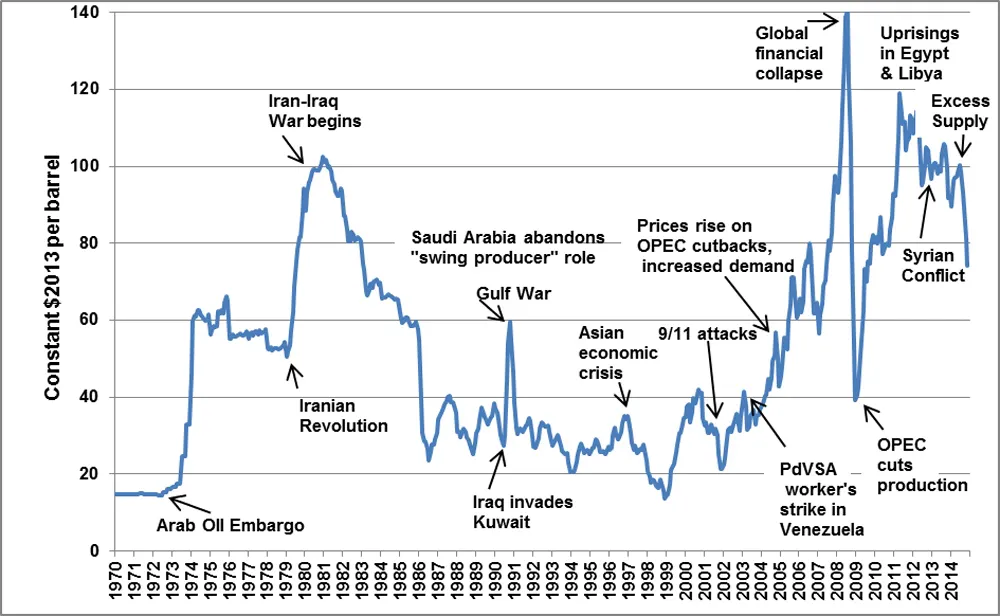

The latest global oil shock is less a spike than a structural tremor that keeps rattling every trade route, policy table, and boardroom forecast. Prices are oscillating between tight supply and brittle demand while conflicts keep choking key chokepoints. Investors who bet on a smooth glide into electrification now face a whiplash reality: OPEC+ discipline, sanctioned barrels finding backdoors, and strategic reserves no longer bottomless. Importers from Asia to Europe are scrambling for redundancy, and producers from the Gulf to the Permian see leverage they have not held in years. This is not a rerun of 1973; it is a rewiring of incentives that will define energy security for a decade.

- Supply security beats price stability as the new policy north star.

OPEC+cohesion and shadow barrels keep market balances opaque.- Strategic reserves and LNG buildouts are the stopgaps, not the finish line.

- Energy transition narratives now compete with raw geopolitics for capital.

How the global oil shock resets power

Every global oil shock shifts leverage, but today the swing factors are different: sanctions reroute flows, freight rates stay elevated, and commodity traders are now de facto diplomats. The interplay between WTI volatility and policy-driven demand destruction means consuming nations cannot simply wait out the storm. Instead, they are renegotiating long-term contracts, hedging with refined product stockpiles, and leaning on bilateral deals outside formal alliances. For producers, restrained spending has tightened supply capacity, giving state-backed exporters pricing power while keeping private operators disciplined.

Supply chains are rerouting in real time

Russian barrels under price caps still move, but at a logistics premium that strains tanker availability. LNG cargos compete with crude for shipping, creating cross-commodity bottlenecks. Refiners in India and China are arbitraging discounts into refined product exports, effectively exporting embedded subsidies to Europe and Africa. Meanwhile, US Gulf Coast refiners juggle export pulls against domestic gasoline politics. The result: benchmarks split and localized shortages flare even when headline inventories look healthy.

OPEC+ discipline versus fiscal pressure

Riyadh and Moscow keep extending voluntary cuts to defend a price floor, but their fiscal breakevens diverge. Saudi Arabia needs sustained triple digits to fund Vision 2030, while Russia needs cash to finance conflict. The cohesion inside OPEC+ hinges on market share math: every extra barrel risks undercutting price support, yet prolonged tightness accelerates demand destruction and fuels substitution. Smaller members with thin reserves feel the squeeze first, testing the alliance when prices soften.

Strategic reserves lose their shock absorber role

The US SPR drawdowns during the last price spike left inventories at multi-decade lows. Refill plans collide with budget limits and storage maintenance windows. Europe lacks a unified reserve strategy, leaning instead on commercial stocks and mandated minimums. Asia’s consumers are expanding storage capacity, but build rates lag demand growth. Without robust buffers, even modest supply disruptions can trigger outsized price reactions, embedding geopolitical risk into every quarterly forecast.

Demand pivots and the contested energy transition

Electric vehicle adoption, efficiency gains, and fuel switching should blunt long-term oil demand, yet short-term elasticity remains thin. Emerging markets prioritize affordability over emissions, locking in consumption growth even as EV sales accelerate in wealthy regions. Aviation and petrochemicals stay sticky demand centers, and the rebound in travel keeps jet fuel tight. The tension between decarbonization pledges and energy security has pushed governments to run dual-track strategies: subsidize renewables while courting crude supply deals.

Refined products are the new battleground

Governments care about pump prices, not crude benchmarks. Diesel inventories drive freight costs and food inflation, making middle distillates the political stress point. Refining capacity closures in Europe and underinvestment globally mean outages have outsized effects. New megarefineries in the Middle East and Asia rebalance flows, but regional specification rules and limited pipelines keep the system fragile. Expect more export controls on fuels when domestic prices spike.

Capital allocation under duress

Upstream firms enjoy cash windfalls but remain cautious. Shareholder pressure for buybacks and dividends trumps growth capex, keeping global spare capacity thin. Meanwhile, ESG screens and financing costs challenge frontier projects. National oil companies fill the gap, but their ambitions depend on political stability and infrastructure integrity. The mismatch between capital discipline and supply needs sets the stage for recurring tightness unless demand declines faster than expected.

Geopolitical fault lines exposed

Energy flows now mirror political blocs. The Atlantic alliance courts producers in Africa and Latin America to diversify away from sanctioned supply. China doubles down on long-term deals with Gulf states and invests in refining joint ventures to lock in product security. India plays both sides, importing discounted crude while seeking Western technology and investment. The Middle East leverages flexible alliances, partnering on LNG, petrochemicals, and renewables to stay indispensable to all parties.

Chokepoints and gray-zone risks

Strait closures, pipeline sabotage, and cyberattacks on terminals are no longer tail risks. Drone strikes on export infrastructure and GPS spoofing in congested lanes add insurance premiums and operational delays. Port congestion from redirected flows adds demurrage costs that show up as higher pump prices. A single incident at a critical junction like the Strait of Hormuz or the Turkish Straits can ripple through freight rates for weeks.

Shadow fleets and opaque pricing

Older tankers moving sanctioned barrels operate outside normal insurance channels, raising environmental and legal exposure. Fragmented data on these flows clouds market transparency, complicating hedging strategies. Price assessments struggle to reflect true differentials when destination and quality data are incomplete. Traders respond with wider risk premiums, and that uncertainty feeds volatility even in otherwise balanced months.

Why this shock is different

Past shocks centered on volume loss; today’s shock is about systemic fragility. Digitized markets react in milliseconds to rumors, while physical barrels need weeks to reroute. Energy transition policies introduce policy-driven demand swings, and climate volatility threatens production with heatwaves and hurricanes. The net effect is a market that can whipsaw between surplus and scarcity without warning.

Policy constraints tighten the vise

Price caps, windfall taxes, and refinery mandates insert political timelines into physical supply chains. Policymakers must balance consumer relief with investment signals, often producing contradictory measures: subsidies that inflate demand alongside regulations that deter supply. The resulting policy noise increases the cost of capital and stretches project timelines.

Technology as a volatility amplifier

Algorithmic trading magnifies intraday swings when headlines break about refinery fires or production cuts. Satellite tracking of tankers adds transparency but also fuels speculative positioning. Meanwhile, digital twins and predictive maintenance reduce downtime for well-funded operators, widening performance gaps between majors and smaller independents.

Playbook for stakeholders

For importers, resilience beats efficiency. Building redundancy through diversified suppliers, flexible contract terms, and regional storage can dampen shocks. Hedging strategies should mix physical and financial tools, while demand-side measures like efficiency standards offer structural relief. For producers, disciplined investment paired with selective capacity expansions can defend market share without crashing prices. Service companies should position around maintenance and debottlenecking, which deliver returns even in volatile price bands.

Pro tips for operators

- Invest in

LNGflexibility to buffer seasonal oil demand spikes. - Use blended pricing formulas tied to both

Brentand refined product indices to smooth volatility. - Prioritize cybersecurity for terminals and pipelines as a core operational risk.

- Align turnarounds with shoulder seasons to avoid peak price exposure.

What investors should watch

Track refinery utilization, shipping rates, and product cracks more than headline crude prices. Monitor policy shifts on subsidies and strategic reserve refills. Watch capital expenditure guidance from state firms versus independents to gauge future supply elasticity. And do not ignore climate-driven production risks: hurricanes in the Gulf Coast or heat-related outages in Middle Eastern fields can swing balances faster than demand forecasts adjust.

Future outlook: contested transition

The next decade will test whether demand reduction can outrun supply constraints. If EV adoption and efficiency gains accelerate, producers may compete for a shrinking pie, pushing prices into a volatile lower band. If emerging market demand stays strong and supply investment remains cautious, the world faces a series of rolling tight markets. Either way, the policy dance between energy security and decarbonization will set the cadence.

Key insight: The countries that marry supply diversification with aggressive efficiency gains will own the new energy map, regardless of where prices settle.

The most likely scenario is a dual-speed system: advanced economies balancing electrification with strategic hydrocarbons, and emerging economies optimizing for affordability with mixed fuels. Companies and countries that build optionality – flexible terminals, modular refineries, agile supply contracts – will navigate the turbulence. Those betting on a single pathway risk being stranded by the next shock.

The information provided in this article is for general informational purposes only. While we strive for accuracy, we make no guarantees about the completeness or reliability of the content. Always verify important information through official or multiple sources before making decisions.