SpaceX IPO Pressure Builds

SpaceX IPO Pressure Builds

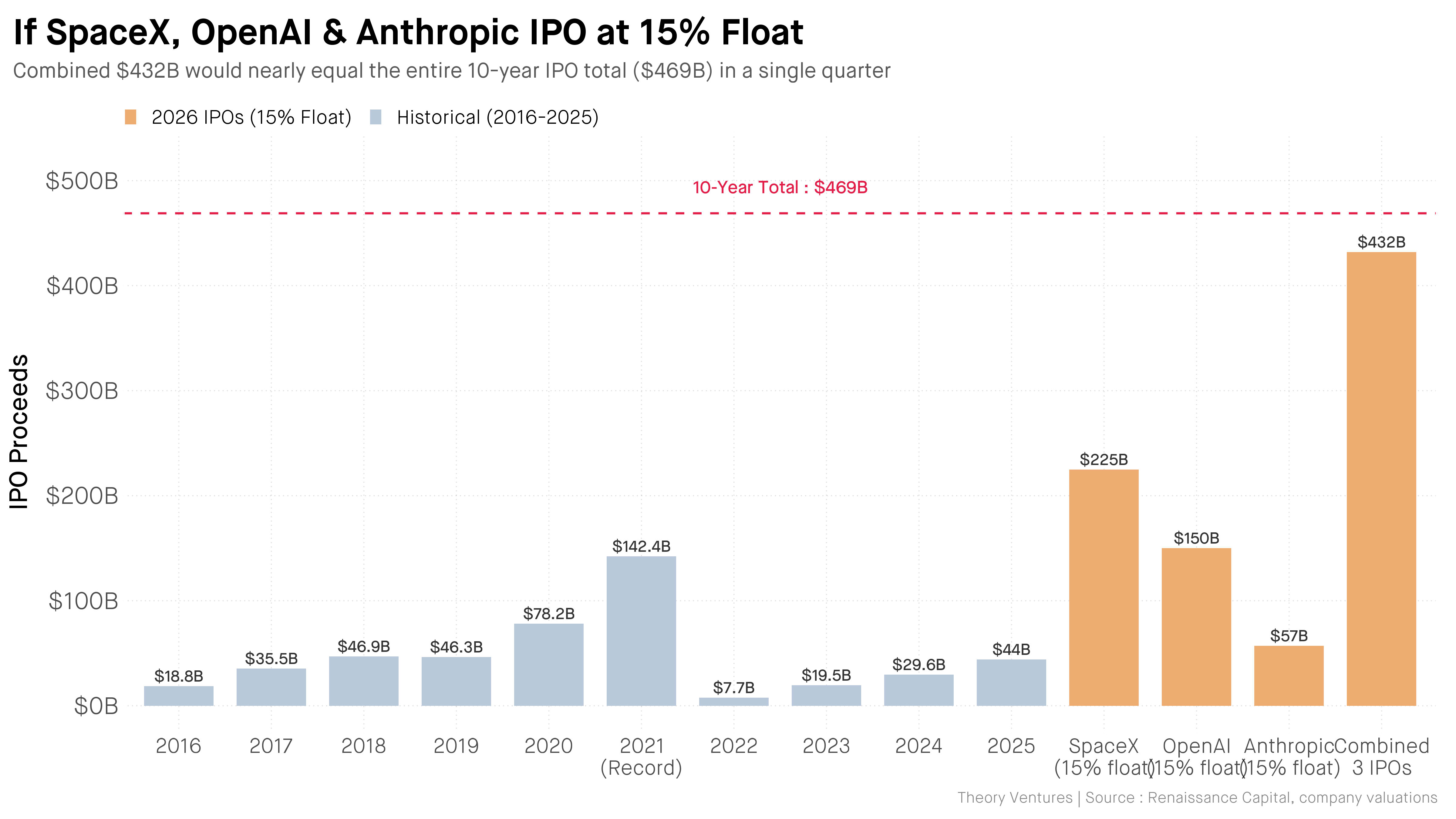

SpaceX IPO pressure is no longer a niche investor fantasy – it is now a governance fight with real institutional muscle behind it. New York City Comptroller Brad Lander, New York State Comptroller Thomas DiNapoli, and CalPERS CEO Marcie Frost have publicly urged SpaceX to consider going public, arguing that one of the most important companies of the modern era should not remain effectively locked away from ordinary investors. That demand lands at a volatile moment: private markets are flush, Elon Musk remains deeply allergic to outside scrutiny, and retail investors are increasingly shut out of the most valuable growth stories until much of the upside is already gone. The bigger issue is not just whether SpaceX lists shares. It is whether the private-capital era has gone too far in concentrating wealth creation among insiders, elite funds, and secondary-market specialists.

- Public pension leaders want broader access to SpaceX through a possible IPO.

- SpaceX IPO pressure highlights a larger debate over private-market exclusivity and public-market fairness.

- SpaceX has strong reasons to stay private, including control, flexibility, and insulation from quarterly scrutiny.

- An IPO would reshape access to one of the world’s most strategically important aerospace companies.

- The fight is as much about governance and market structure as it is about Musk.

Why SpaceX IPO pressure matters now

The public letter is notable because it does not come from impatient retail traders or speculative finance media. It comes from leaders who represent massive pools of retirement capital. That matters. These institutions are effectively saying the current arrangement leaves long-term public investors on the outside while private insiders capture disproportionate value.

SpaceX is not a normal startup hanging onto privacy while it finds product-market fit. It is a dominant launch provider, a major defense contractor, a satellite internet operator through Starlink, and arguably one of the most strategically significant private companies in the United States. When a company reaches that level of scale and influence, calls for broader accountability become harder to dismiss as mere market noise.

The underlying message is simple: if a company benefits from public infrastructure, public contracts, and public policy, pressure for public accountability tends to follow.

That does not mean SpaceX is obligated to list tomorrow. But it does mean the argument for permanent private status is getting weaker as the company becomes more central to communications, defense, and industrial policy.

The case for a SpaceX IPO

Broader investor access

The most obvious argument is fairness. SpaceX has become one of the defining companies of the era, yet most ordinary investors cannot buy in directly. Access is largely limited to private funding rounds, insider liquidity programs, or indirect exposure through funds and suppliers. By the time many elite companies finally go public, the steepest growth curve has already passed.

That is a sore point for pension managers. Their beneficiaries are everyday workers, and those workers increasingly miss the wealth-creation phase that once happened in public markets. A SpaceX listing would not solve that structural imbalance by itself, but it would become a high-profile test case.

Governance and disclosure

Public markets impose burdens, but they also impose discipline. A listed SpaceX would face recurring reporting requirements, greater transparency around risks, and more formal accountability to outside shareholders. For a company with massive public relevance, that is not a trivial benefit.

Investors would gain clearer insight into segments like launch services, government contracts, and Starlink subscriber economics. Analysts could better assess capital intensity, operating margins, and cash flow durability. Right now, much of that remains opaque or filtered through fundraising narratives.

Liquidity for employees and early investors

As private companies stay private longer, liquidity becomes a governance issue. Employees may receive compensation tied to equity yet have limited opportunities to realize value. Secondary programs help, but they are controlled events, often priced on terms set by the company. An IPO would broaden liquidity and create a more transparent market for price discovery.

Why SpaceX may resist going public

For all the pressure, the anti-IPO argument remains strong. And SpaceX has more leverage than most companies because it already has what everyone else wants: capital access, customer demand, strategic relevance, and a founder who is comfortable ignoring convention.

Control is the real currency

Elon Musk has repeatedly shown that he values control over nearly everything else. Public markets bring analysts, activist investors, headline-driven volatility, and a constant demand for disclosure. For a company pursuing long-horizon bets in rocketry, satellite broadband, and possibly Mars infrastructure, that can look like strategic friction rather than healthy oversight.

Remaining private allows SpaceX to manage product timelines, tolerate experimental failure, and allocate capital without the theater of quarterly earnings calls. That freedom is especially valuable in aerospace, where timelines slip, programs evolve, and technical setbacks are part of the model.

Private capital is still abundant

The classic reason to go public used to be simple: companies needed the money. That logic has weakened. Today, elite private firms can raise enormous rounds at extraordinary valuations. If SpaceX can secure capital without public disclosure and without ceding meaningful control, the incentives to list are limited.

This is the heart of the modern market problem. Public investors want access, but private companies often do not need them.

Musk knows the costs of public scrutiny

Musk already runs public companies and has spent years in open conflict with regulators, critics, short sellers, and governance watchdogs. He does not need a tutorial on the downsides of listing. If anything, his experience likely reinforces the appeal of keeping SpaceX outside that machinery for as long as possible.

For Musk, an IPO is not just a financing event. It is an invitation to surrender time, narrative control, and strategic secrecy.

What the pension funds are really saying

The letter is not just about adding another ticker to the market. It is about who gets to participate in modern wealth creation. Public pensions are signaling frustration with a system in which transformational companies can remain private deep into maturity, leaving retirement savers with narrower opportunities and later-stage entry points.

There is also a policy undertone here. SpaceX is intertwined with national priorities: launch capacity, space infrastructure, military communications, and broadband resilience. When private concentration gets that intense, public stakeholders start asking whether market access and disclosure standards should evolve too.

The institutional investor perspective

Large pension systems are long-duration investors. They are not looking for meme-stock volatility. They want exposure to durable growth, strategic industries, and category leaders. SpaceX fits that template almost perfectly. Their push for an IPO reflects a belief that public markets should still be the place where major economic value is shared broadly.

Pro tip: When pension leaders make a public governance argument, it is usually aimed at the broader market as much as the company itself. The intended audience often includes regulators, policymakers, and other institutional investors.

How a SpaceX IPO could actually happen

If SpaceX ever moves, it may not be through a conventional all-at-once flotation. There are several paths, each with trade-offs.

- Traditional IPO: The cleanest route for broad public access, but also the heaviest in terms of process and disclosure.

- Direct listing: Could provide liquidity without a standard capital raise, though it is less common for a company with SpaceX’s profile and needs.

- Partial spinout: A separate listing of

Starlinkhas long seemed more plausible than floating the full SpaceX business. - Expanded secondary access: Not a true IPO, but a compromise path that widens liquidity while preserving private status.

A Starlink listing may be the most realistic middle ground. It offers a more legible consumer and telecom-style story for public investors while letting the core launch and deep-space operations remain more tightly controlled. That said, even a spinout would raise familiar questions about governance, intercompany dependencies, and transfer pricing.

What investors should watch next

Signals from management

Watch for any softening in rhetoric around public ownership, especially if management begins emphasizing liquidity, employee retention, or segment-specific transparency. Those are often early signs that internal conversations are evolving.

Valuation behavior in private rounds

If private financing remains easy and valuations stay elevated, the urgency for an IPO stays low. If capital conditions tighten or pricing becomes less forgiving, public markets become more attractive.

Regulatory and political momentum

If more public officials and pension systems amplify this argument, the conversation could shift from polite suggestion to broader policy debate. That would not force SpaceX public, but it could increase pressure around disclosure, access, and governance norms for mega-scale private companies.

The bigger market problem behind SpaceX IPO pressure

This is the part that should concern more than just aerospace enthusiasts. The SpaceX debate is really a referendum on whether public markets still serve their historic function. For decades, the stock market was where ordinary investors could participate in the rise of major companies before all the value had already been harvested. That bargain has eroded.

Today, late-stage private capital lets companies delay listing almost indefinitely. The result is a more exclusive ownership model, one that rewards insiders, sovereign wealth, venture firms, and giant asset managers while shrinking direct participation for everyone else. SpaceX is simply the highest-profile example because the company is so consequential and the founder is so impossible to ignore.

If SpaceX eventually goes public, it will not just be a blockbuster listing. It will be a symbolic test of whether the public market still has a claim on the future.

Final verdict on SpaceX IPO pressure

The pension leaders pressing SpaceX are making a serious point, and they are making it at the right time. SpaceX has grown beyond the usual startup exceptions. Its reach is industrial, geopolitical, and consumer-facing. The argument that ordinary investors deserve a path to ownership is compelling, especially when public institutions already underpin so much of the environment in which the company operates.

Still, moral clarity does not automatically create strategic incentives. As long as SpaceX can raise private capital, protect founder control, and avoid the noise of public-market life, resistance will remain rational. That is why SpaceX IPO pressure matters even if no filing appears soon. It exposes a deeper fracture in modern capitalism: the most important companies increasingly shape public life while staying financially distant from the public itself.

If that sounds unsustainable, it probably is. The only real question is whether SpaceX becomes the company that finally proves it.

The information provided in this article is for general informational purposes only. While we strive for accuracy, we make no guarantees about the completeness or reliability of the content. Always verify important information through official or multiple sources before making decisions.