Canada Targets Crypto ATM Crime

Canada Targets Crypto ATM Crime

Crypto ATMs were supposed to make digital money feel as easy as grabbing cash from a corner machine. Instead, they have become a pressure point for fraud investigators, anti-money laundering teams, and policymakers trying to keep up with a fast-moving financial system. Now Canada is moving to build a new financial crimes agency at a moment when concern is growing that the US is dialing back parts of its enforcement posture. That combination matters. Criminal networks do not care about borders, and neither does dirty money when it can move through cryptocurrency ATMs, shell accounts, and loosely monitored cash-to-crypto channels. For consumers, the risk is direct and personal. For regulators, it is structural. And for the crypto industry, this is another test of whether convenience can coexist with accountability.

- Canada is sharpening its response to financial crime with a new agency aimed at stronger enforcement capacity.

- Crypto ATM crime has emerged as a serious concern because these machines can be exploited for fraud and money laundering.

- A weaker US stance could create cross-border enforcement gaps that sophisticated actors quickly exploit.

- Legitimate crypto businesses may face tighter compliance expectations as regulators target high-risk access points.

- Consumers need more protection because scams often use

crypto ATMsas the final step in irreversible payments.

Why Canada is moving now on crypto ATM crime

The timing is not accidental. Canadian officials are responding to a familiar pattern: financial innovation arrives first, criminal exploitation follows fast, and regulation catches up under pressure. Crypto ATM crime sits right in that gap. These kiosks offer a simple bridge between cash and digital assets, but that same simplicity can make them attractive to scammers who want victims to convert money quickly and send it to wallets beyond easy recovery.

The policy concern is bigger than one machine in one convenience store. Regulators increasingly see crypto ATMs as part of a broader risk environment that includes romance scams, impersonation fraud, ransomware cash-outs, and laundering networks that fragment transactions to avoid detection. A new financial crimes agency gives Canada a way to centralize expertise, coordinate intelligence, and move faster when old enforcement structures are too fragmented.

The real issue is not whether crypto is legal. It is whether regulators can see, stop, and punish abuse before trust in the system breaks down.

That is the strategic backdrop. If the US eases off while Canada tightens up, enforcement asymmetry becomes the story. Criminal actors tend to route activity through the weakest link, then use international complexity as cover.

How crypto ATMs became such a hot spot

At first glance, a crypto ATM looks mundane: a touchscreen, a payment flow, a promise of easy access. But ease is exactly what makes these machines vulnerable. Many scam operations do not need advanced cyber exploits. They need a frightened victim, a believable script, and a payment rail that is fast and hard to reverse.

The scam playbook is brutally simple

A victim receives a call, text, or pop-up message claiming their bank account is compromised, their taxes are overdue, or a family member needs urgent help. The fraudster instructs them to withdraw cash, go to a nearby cryptocurrency ATM, and send funds to a wallet controlled by the criminal. By the time the victim realizes what happened, the money has likely moved through multiple addresses.

That is why crypto ATM crime is not just a regulatory talking point. It is a consumer protection crisis dressed in fintech language.

Money laundering risk is built into the access model

Even where operators follow rules, these machines can present obvious risk factors: cash-based transactions, varying identity checks, uneven monitoring standards, and fragmented oversight. Bad actors look for volume, speed, and opacity. A kiosk network with weak compliance can offer all three.

To be clear, this does not mean every crypto ATM is inherently illicit. It means the sector carries elevated risk and therefore demands elevated controls.

What a new Canadian financial crimes agency could change

Governments often announce new institutions with big rhetoric and limited follow-through. The success of Canada’s plan will depend less on branding and more on execution. If the agency can combine intelligence, licensing scrutiny, enforcement, and interagency cooperation, it could materially reshape how crypto ATM crime is investigated.

Expect tighter compliance pressure

Operators may face more aggressive expectations around know-your-customer checks, suspicious transaction reporting, transaction caps, machine placement reviews, and real-time monitoring. Regulators may also push for stronger wallet screening tools and faster information-sharing between local police, federal agencies, and financial intelligence units.

For compliant businesses, that will be costly. But the alternative is worse: an entire category of crypto access points becoming synonymous with fraud.

Data and coordination matter more than headline raids

One underappreciated point in any anti-money laundering strategy is that dramatic takedowns are less important than routine visibility. Authorities need cleaner data, better pattern recognition, and the ability to connect isolated incidents into a network map. A capable agency can spot links between scam reports, wallet clusters, cash deposits, and machine operators before a problem scales nationally.

Pro tip for operators: if your compliance system relies mostly on after-the-fact reviews, you are already behind. Higher-risk channels need intervention during the transaction, not after it settles.

Why the US policy shift matters to Canada

Canada is not operating in a vacuum. If the US weakens parts of its approach to crypto oversight, Canadian regulators may have to compensate. Cross-border financial crime thrives when rules are inconsistent, priorities diverge, or agencies send mixed signals to the market.

That does not necessarily mean the US has abandoned enforcement. It means even modest softness in posture can have outsized signaling effects. Markets hear it. Operators hear it. Criminals definitely hear it.

Enforcement gaps are rarely local for long. In digital finance, a softer neighboring regime can become your problem almost overnight.

The geography of financial crime has changed

Traditional anti-money laundering frameworks were built around banks, branches, and national jurisdictions. Crypto networks break those assumptions. A scam can begin on a social platform, end at a crypto ATM in Canada, hit a wallet hosted elsewhere, and be dispersed through services in multiple countries within minutes.

That is why Canada’s move is as much about resilience as law enforcement. If one major jurisdiction loosens its grip, others need sharper tools to avoid becoming spillover zones.

What this means for the crypto industry

This is the uncomfortable part for crypto advocates: every consumer scam tied to a kiosk damages the industry’s legitimacy. The promise of open financial infrastructure sounds compelling until ordinary users associate it with coercion, loss, and zero recourse.

Companies that want mainstream adoption should not treat tougher oversight as an existential threat. They should treat it as market hygiene. Better controls can help separate serious operators from opportunists.

There is a path forward for legitimate players

- Stronger identity verification: Risk-based onboarding should be standard, not optional.

- Behavior monitoring: Repeated cash deposits, rapid wallet changes, and unusual transaction timing should trigger intervention.

- Consumer warnings: Machines should clearly flag common scam scripts before a user sends funds.

- Location discipline: High-risk placement strategies may invite extra scrutiny from regulators.

- Faster reporting: Escalation workflows should be built for minutes, not days.

In practical terms, this may also push more operators to harden their internal systems with controls like transaction velocity limits, wallet risk scoring, and alert-based case management.

How consumers can protect themselves from crypto ATM crime

The technology is not the only issue. Human vulnerability is the attack surface scammers exploit most effectively. That makes consumer education essential.

Warning signs that should stop any transaction

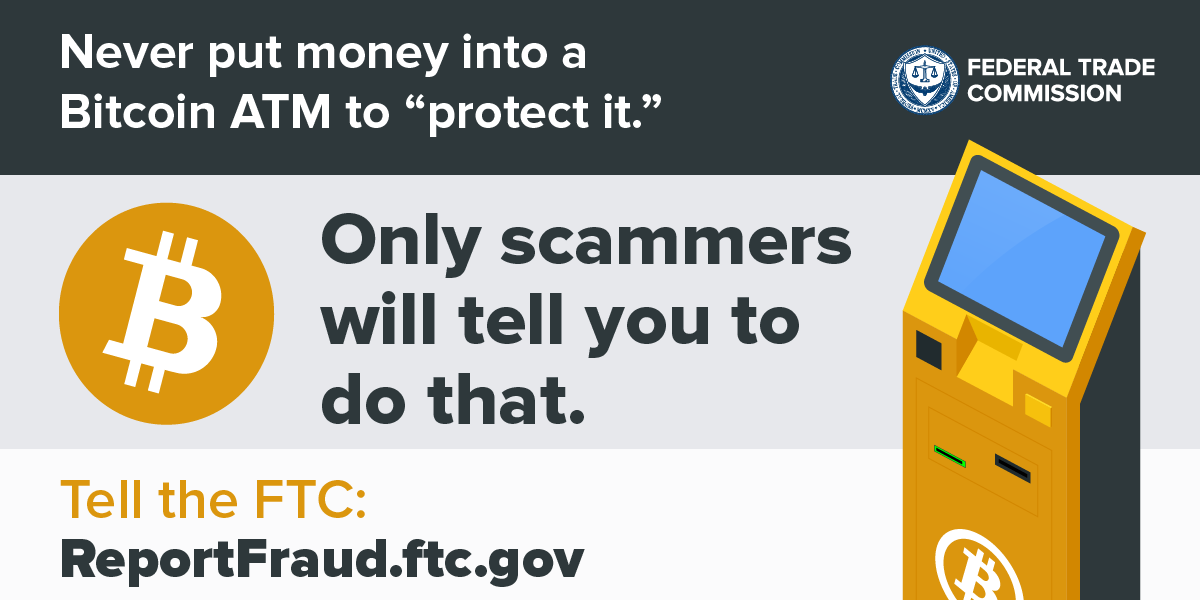

- Someone tells you to pay a bill, fee, or fine using a

crypto ATM. - You are being rushed by a caller claiming urgency or secrecy.

- The payment is framed as protective, such as moving money to a so-called safe wallet.

- You are asked to ignore bank staff, family, or police advice.

- The recipient cannot be independently verified.

If any of those conditions appear, the safest move is simple: stop. A legitimate government agency, utility, or bank does not require emergency payment through cryptocurrency ATMs.

A practical rule worth remembering

If someone you do not know is telling you exactly how to buy crypto and where to send it, you are almost certainly being manipulated. That single rule would prevent a remarkable amount of loss.

Why this matters beyond Canada

The broader story here is not only about kiosks. It is about whether democratic governments can update financial safeguards quickly enough for hybrid systems where cash, software, and global networks interact in real time. Crypto ATM crime just happens to be a visible symptom.

If Canada gets this right, it could become a model for targeted, risk-based oversight that protects consumers without collapsing legitimate innovation. If it gets it wrong, the likely outcomes are familiar: heavier fraud losses, more public distrust, and eventually more blunt regulation.

There is also a political dimension. Financial crime policy increasingly sits at the crossroads of security, technology, and economic competitiveness. A government that cannot police modern payment rails looks reactive. A government that overreaches risks choking off useful innovation. The skill is in precision.

The next phase of crypto regulation will not be defined by ideology. It will be defined by who can reduce harm while preserving credible room for innovation.

The bottom line on crypto ATM crime

Canada’s planned financial crimes agency is a signal that policymakers no longer see crypto ATMs as a niche issue. They see them as a frontline enforcement challenge tied to fraud, laundering, and cross-border regulatory drift. That is a rational shift. These machines may offer convenience, but convenience without oversight is exactly what bad actors monetize.

The industry should pay attention. Consumers should be cautious. And regulators in other countries should treat this as an early warning, not a local oddity. The future of digital finance will depend less on how fast money can move and more on whether the systems around it can tell the difference between access and abuse.

The information provided in this article is for general informational purposes only. While we strive for accuracy, we make no guarantees about the completeness or reliability of the content. Always verify important information through official or multiple sources before making decisions.